On September 23, Haier’s Chonburi Air Conditioner Industrial Park in Thailand officially began production. The park has a planned annual capacity of 6 million units and covers multiple categories of air-conditioning products. On the same day, Hisense held a groundbreaking ceremony for its HHA Smart Manufacturing Industrial Park in the Amata City Chonburi Industrial Estate, Thailand. The HHA park will be developed in three phases and is expected to be fully completed by 2030, with an estimated annual production capacity of 2.6 million units once fully operational.

10 Days after, on October 6, the BOI (Thailand Board of Investment) approved the investment application for Omar to establish a refrigerator production base in Thailand. The first phase of the project involves an investment of 3 billion Thai Baht to build an intelligent refrigerator and freezer factory with an annual output of 1.7 million units, mainly for export to the European market.

Together with existing production capacities established by Japanese and Korean brands such as Panasonic, Toshiba, Hitachi, LG, and Samsung, Chinese, Japanese, and Korean home appliance giants have now all gathered in Thailand. Behind this clustering of production lines lies a new wave of global supply chain restructuring.

Industry insiders point out that Chinese home appliance enterprises’ enthusiasm for “going south” to Southeast Asia essentially represents a process of “restructuring.” The core strategic goal is to reallocate production capacity and optimize cost structures on a global scale, driving companies to advance toward a new stage of “global manufacturing and global sales.”

Car Companies Go First: Thailand becomes the “manufacturing springboard” of Southest Asia.

The intensive expansion of Chinese brands in Thailand did not come as a surprise.

Several years ago, Chinese automakers such as BYD, Changan, and Foton had already begun establishing their presence in Thailand, becoming deeply integrated into the country’s automotive industrial chain.

If we look back five years, Chinese-brand vehicles were still a rare sight on Thai streets.

But today, driving from Suvarnabhumi Airport toward downtown Bangkok, one can see billboards for SAIC MG, GAC Aion, BYD, and Great Wall Motors lined up along the highways.

The data is more compelling, According to the CAAM (China Association of Automobile Manufacturers), in 2024, Thailand became China’s fourth-largest export destination for new energy vehicles (NEVs)—after Belgium, Brazil, and the United Kingdom. That year, China exported 178,000 NEVs to Thailand, a year-on-year increase of 35%, accounting for one-quarter of Thailand’s total automobile imports.

To better serve local consumers, by the end of 2024, seven Chinese carmakers had established operations in Thailand. In addition to BYD, Changan, and Foton, brands such as SAIC MG, Great Wall Motors, and GAC Aion have also set up shop—creating a complete ecosystem from planning and production to sales.

Thailand’s rise as a major manufacturing hub is no coincidence. Strategically located in the heart of Southeast Asia, Thailand borders Malaysia to the south, Cambodia to the east, and Myanmar to the west, while its northern region connects to China’s Yunnan province and its southern position controls the entrance to the Strait of Malacca. Even more importantly, Thailand enjoys relatively strong political stability and policy continuity.

The emergence of Laem Chabang Port has been key to Thailand’s manufacturing boom. As a deep-water port on Bangkok Bay, Laem Chabang has been in operation since 1991 and is now the second-largest container port in Southeast Asia. With over 100 international shipping routes each week connecting it to major ports worldwide, it provides an irreplaceable competitive advantage for manufacturers that rely on imported raw materials and exported finished products.

In addition to favorable geography, low production costs are another reason automakers choose Thailand.

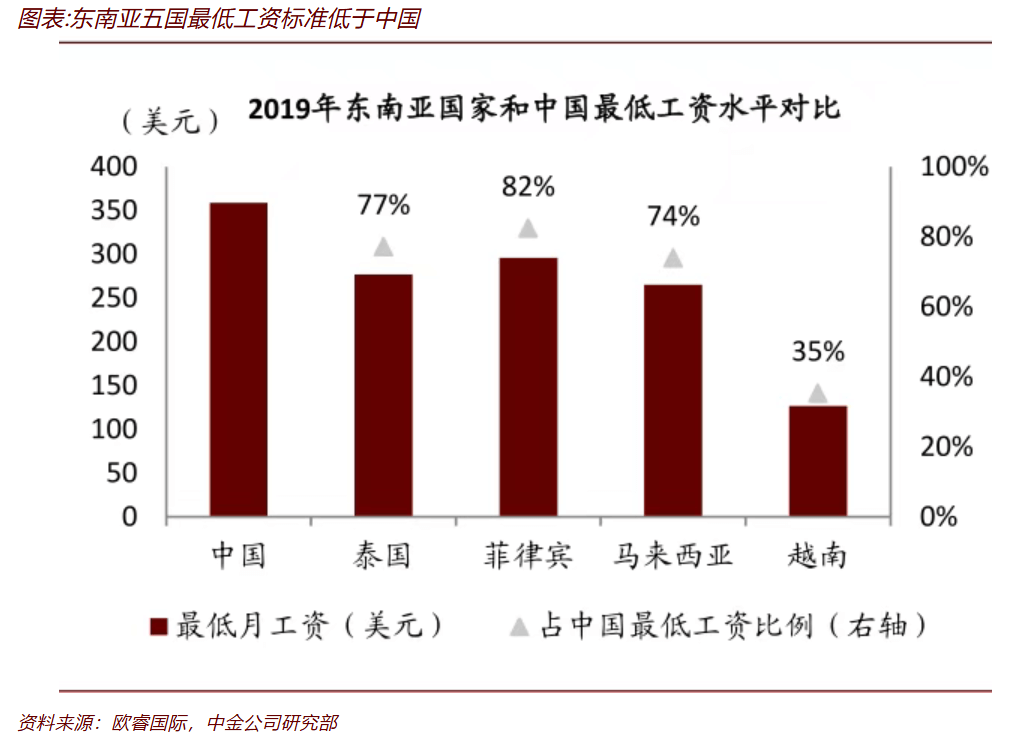

A report from CICC notes that the average weekly working hours in China are 46 hours, while in Thailand they are 45 hours—roughly comparable. According to Euromonitor data, in 2019 Thailand’s minimum monthly wage was about 77% of China’s. Combined with a relatively skilled workforce and a certain level of English proficiency, Thailand is highly attractive for foreign companies looking to invest in local manufacturing.

From left to right: China, Thailand, Philippines, Malaysia, Vietnam.

As of 2023, Thailand’s automobile production accounted for 45% of total ASEAN vehicle output, cementing its position as the automotive hub of Southeast Asia. Thailand has also entered the ranks of the world’s top ten automobile producers, surpassing traditional industrial powers such as France and the United Kingdom.

The “produce locally, sell locally” model has helped Chinese automakers quickly gain market share in Thailand. Chinese brands hold a particularly strong advantage in the pure electric vehicle (EV) segment. In the first three quarters of 2025, Thailand registered 86,432 new EVs, with BYD (including Denza) leading at 29,633 units, capturing 34.3% of the EV market. GAC Group (Aion + HYPTEC) and Changan Group (Deepal + AVATR) followed with 9,579 and 8,884 units, respectively. MG, Great Wall’s Ora, and others also made the top five; among the top ten best-selling EVs, seven are Chinese brands.

Chinese automakers’ focus on Thailand has also been influenced by Japanese automakers’ longstanding presence. Thailand has long been a key base for Japanese brands. From the mid-20th century (1960s–1980s), Japanese automakers expanded their market in Southeast Asia primarily through vehicle exports, gradually establishing a strong regional footprint. As many countries began raising import tariffs and trade barriers, coupled with the appreciation of the yen after 1985, export costs increased, prompting Japanese companies to set up overseas production facilities—Thailand became their preferred choice.

By the 21st century, Japanese automakers had developed a mature global layout, establishing production bases and sales networks in multiple countries and regions. Domestic exports have remained around 3–4 million vehicles per year, while overseas production has risen to nearly 17 million vehicles annually, roughly four times the domestic export volume.

Thanks to this “three-step” strategy, Japanese brands have rapidly expanded their coverage in Thailand and Southeast Asia. By the end of 2023, Japanese cars accounted for 68.1% of the Southeast Asian automotive market. In key markets such as Indonesia, Thailand, and the Philippines, the combined market share of Toyota and Honda reached 69%, 45%, and 50%, respectively.

Moreover, the 20+ years of Japanese production presence in Thailand has cultivated a large pool of skilled manufacturing talent, providing favorable conditions for other automakers—including Chinese brands—to follow.

According to the Thailand Board of Investment (BOI), in 2024, Chinese enterprises applied for $5.1 billion in direct investment in Thailand, an increase of 10% year-on-year, surpassing Japan and the United States and ranking first among Thailand’s major trade partners.

Home Applience Companies picked up the baton: Why Now?

The layout of Japanese home appliance companies in Thailand has also served as an inspiration for Chinese enterprises.

As early as 1979, Panasonic had already started producing washing machines and refrigerators in Thailand. In 1988, Sharp established a factory in Thailand, manufacturing products including refrigerators, air conditioners, and washing machines. In the 1990s, Hitachi also began its operations in Thailand by founding HADSYS (Thailand) Co., Ltd., primarily engaged in the production and sales of refrigerator compressors.

The second wave of factory construction in Thailand has been concentrated in the past decade. In May 2012, Toshiba launched plans for a second production facility in Thailand. Later that November, Toshiba announced the establishment of a joint venture in Thailand to produce core air-conditioning components, including compressors.

The reason behind this phenomenon is the rapid growth of home appliance demand in Southeast Asia, particularly for traditional “big three” appliances, with air conditioners still seeing substantial growth overseas. According to Euromonitor, the CAGR of the home appliance market in six Southeast Asian countries from 2018 to 2023 was 5%, with penetration levels roughly equivalent to China around 2010. Considering domestic growth rates and price differences as benchmarks, Euromonitor predicts that the Southeast Asian home appliance market could achieve 5–10% growth in the coming years.

Moreover, many Southeast Asian countries are in tropical regions with hot climates, driving exceptionally strong demand for air conditioners, refrigerators, and washing machines. For example, in Bangkok, the capital of Thailand, the annual average temperature is 27.5°C, with highs exceeding 40°C. Yet only 50.9 out of every 100 households own an air conditioner, indicating enormous potential for growth. This explains why companies like Haier and Hisense have prioritized locating air-conditioner production lines in Thailand.

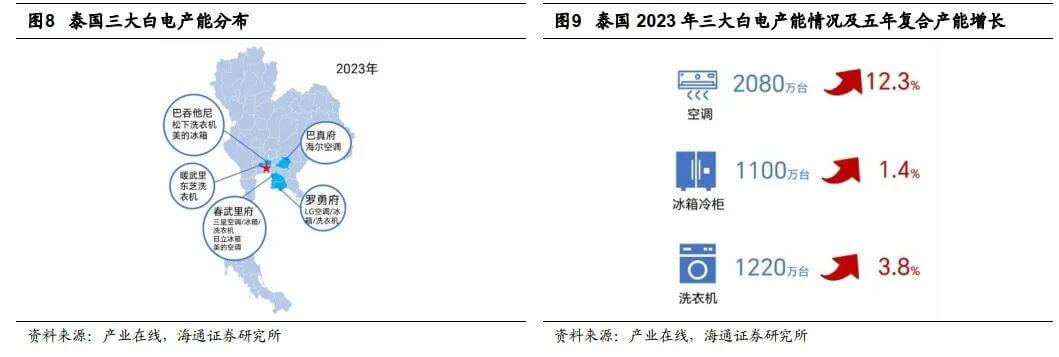

According to Haitong Securities, Thailand is now the largest white-goods manufacturing country in Southeast Asia. Over the years, major manufacturers from Japan, Korea, and China have successively established factories there, making Thailand the second-largest global white-goods producer outside China. This is largely due to the recent restructuring of the global home appliance manufacturing supply chain, with Thailand successfully absorbing factory capacity relocated from Japan, Korea, and China.

Chen Ziyi, Chief Analyst of Home Appliance Research at Haitong Securities, noted that looking at the competitive landscape in Southeast Asia, Korean brands still hold a leading position, followed by Japanese brands. As Chinese companies gradually acquire overseas brands (such as Toshiba) and establish related factories in Southeast Asia, Chinese brands are steadily gaining market share in regions such as Indonesia, Thailand, and Vietnam.

Except in developed countries like Singapore, where domestic brands have relatively low market share, Chinese brands enjoy high acceptance in the other five Southeast Asian countries. By product category:

- Televisions: Chinese brands (including acquired brands) hold nearly 30% market share in Indonesia and Thailand.

- Refrigerators and washing machines: Chinese brands (including acquired brands) account for over 15% of the market in Indonesia, Thailand, Malaysia, and Vietnam.

- Air conditioners: Chinese brands (including acquired brands) have a sales share exceeding 20% in Indonesia, Thailand, Malaysia, and Vietnam.

Changes in the trade environment have also accelerated decision-making cycles for home appliance companies.

In its investment documents, Omar Appliances explicitly states that its Thailand factory will “primarily export to Europe.” This is no coincidence. In recent years, Europe has imposed high anti-dumping tariffs on Chinese refrigeration products, whereas exports from Thailand benefit from the ASEAN–EU Free Trade Agreement, significantly reducing tariff costs. The same logic applies to the U.S. market, where ongoing trade tensions have pushed companies to seek “third-country” production sites.

Policy incentives and supply-chain integration advantages are also significant. Since the implementation of the Regional Comprehensive Economic Partnership (RCEP), tariff reductions and origin rules within the region have greatly lowered trade costs. To attract more foreign investment, Thailand has introduced corresponding incentives, including tax reductions, local procurement benefits, streamlined production regulation, investment guidelines, and foreign employment policies. For high-end manufacturing industries such as home appliances and automobiles, Thailand even offers ultra-low corporate tax rates as low as 5%.

Combining market advantages, policy incentives, existing industrial strengths, and a skilled labor force, Chinese home appliance companies have chosen this moment to expand aggressively into Thailand, making their timing particularly opportune.

From “Going out” to “Going Up”: The 3 Stages of “Made in China”.

This migration of home appliance companies is, in fact, a microcosm of the “Made in China” global expansion journey.

Overall, Chinese home appliance exports can be divided into three stages:

1. Product Export Era (2000–2010): During this stage, Chinese companies relied on relatively low-cost yet efficient labor, gaining a strong cost advantage and rapidly expanding contract manufacturing. The market was characterized by high production volume but low brand recognition, a trend that continues today. By 2020, China accounted for roughly 70% of global air conditioner production, 50% of refrigerators, and 40% of washing machines. At that time, Chinese companies mainly sold products overseas through trade, and “Made in China” was largely synonymous with affordable yet high-quality goods.

2. Brand Export Era (2010–2015): During this period, assembly operations were relocated to Southeast Asia and other regions, though core components continued to be imported from China. While this reduced costs, it created a somewhat awkward “two ends outside” situation—materials abroad, markets abroad, only assembly local.

3. Capability Export Era (2020–present): In this stage, Chinese companies have shifted from focusing solely on overseas sales to building capabilities across the full value chain, including R&D, supply chain, and marketing. In R&D, 78% of surveyed companies have either deployed or plan to deploy overseas R&D operations in the near term. In supply chain management, Chinese firms are leveraging domestic strengths to build international flexible supply chains.

In short, Chinese companies’ global expansion is evolving from “going out” → “going in” → “going up”: expand abroad, penetrate mainstream markets, and ultimately become leading brands.

At Haier’s Chonburi Air Conditioner Industrial Park in Thailand, we see more than just production lines—there are R&D centers and sales networks. Engineers develop air conditioners suited to Southeast Asia’s hot and humid climate, while marketing teams study Thai consumer habits to adjust product design and selling points.

For example:

- Observing that Thai consumers enjoy smoothies in the hot summer, Haier developed refrigerators capable of making large ice slushes.

- During the humid rainy season, bacteria can proliferate, so Haier launched self-cleaning air conditioners.

- Considering multi-person households, Haier designed large-drum washing machines.

- This year, Haier debuted an AI smart voice air conditioner that can interact freely without internet, catering to consumers’ desire for convenience.

Deep localization has brought high returns. Haier’s 2024 financial report shows that overseas markets generated RMB 143.814 billion in revenue, up 5.43% year-on-year, with Southeast Asia contributing RMB 6.6 billion, up 14.8% year-on-year.

Thanks to Chinese home appliance companies’ insight into local demand, Chinese brands are gradually taking market share from Japanese brands. HTSEC’s report shows that in 2018, the top three air conditioner brands in Thailand were Mitsubishi, Daikin, and Panasonic. By 2023, Haier entered the top three, and the market share of Chinese brands in this category increased from 13.1% to 21%. The latest 2024 data indicates the top five brands in Thailand’s air conditioner market are Haier, Mitsubishi, Daikin, TCL, and Panasonic, with two Chinese brands now in the top five.

CICC analyst He Wei summarized that in Southeast Asia, refrigerators, washing machines, and major kitchen appliances are largely dominated by Chinese, Japanese, and Korean companies. Japanese brands once held a clear advantage, but in recent years, Chinese companies have significantly increased their share through acquisitions—Haier acquiring Sanyo, Midea acquiring Toshiba, and Taiwan’s Foxconn acquiring Sharp.

A Long-Term Influence: An Endless Relay.

Over the past century, the global consumer appliances and consumer electronics industries have continuously migrated along the path: United States → Japan → South Korea / Taiwan → Mainland China → Southeast Asia / South Asia. Currently, the process is at the stage of Mainland China relocating toward Southeast Asia and South Asia. Among these, the supply chain transfers in consumer electronics and apparel are the most pronounced, followed by consumer appliances.

The success of the “Thailand model” in the automotive industry is creating a demonstration effect. Automakers take the lead, home appliance companies follow closely, and the next likely sectors could be consumer electronics, new energy equipment, or industrial machinery. As the number of manufacturing bases increases, the demand for localized equipment and core components inevitably rises, which will drive more supply chain-related companies to expand overseas.

More importantly, the “Thailand model” is being replicated in other parts of the world. In Mexico, Chinese automakers and home appliance companies are rapidly establishing a presence, targeting the North American market; in Poland, Chinese manufacturers are leveraging local advantages to expand their reach across Europe.

This relay has no finish line. From product exports → capacity exports → capability exports, Chinese manufacturing is writing a new global story. In this story, there are no permanent leaders, only the relay baton being continuously passed.

Dr. Yin Yanlin, economist and academic advisor to the China Finance 40 Forum, defines this global industrial and supply chain migration as “restructuring” in his new book Deep Reform. The book also points out:

“Supply chains are the most powerful link of globalization, but the three-year pandemic accelerated a deep adjustment of global industrial and supply chains. In the past, supply chain relocation had two main drivers: one was cost-driven, the other to bypass trade barriers. In recent years, a third driver has emerged: multinational corporations require suppliers to relocate for risk mitigation. This makes supply chain migration no longer a simple spillover issue, but a forced relocation.”

In other words, this relay of capability export is far from reaching its end. With its strategic location and favorable conditions, Thailand is destined to remain a critical hub on the road of Chinese manufacturing’s global expansion.